F-Gas Regulation and HFC Phasedown

How does the F-Gas regulation affect your business and how you can plan for the future?

Author

Dr Rob Lamb

Group Sales & Marketing Director

The UK's largest independent industrial refrigeration engineering company.

Dr Rob Lamb

Group Sales & Marketing Director

In March 2023, the European Parliament voted for a more aggressive phase-down of hydrofluorocarbon (HFC) gases, aiming for a full phase-out by 2050 and banning HFCs and HFOs in multiple applications from January 2026 and 2027. However, negotiations aren’t expected to include until summer and on 5th April 2023, the European Council brought a more lenient approach, relaxing the quota step-down.

Please view our new updated article to find out more https://www.star-ref.co.uk/smart-thinking/the-new-fluorinated-gas-f-gas-regulation-phase-down-draft-proposal-april-2022/

What are F-gases?

Fluorinated gases are used in a number of applications including refrigeration and air conditioning. When released into the atmosphere they remain there for many years and contribute towards global warming. The F-gas Regulation was introduced in 2006 and included measures to reduce leakage of refrigerants. Following a review of its effect, the regulation was revised in 2014.

F-gas Phasedown

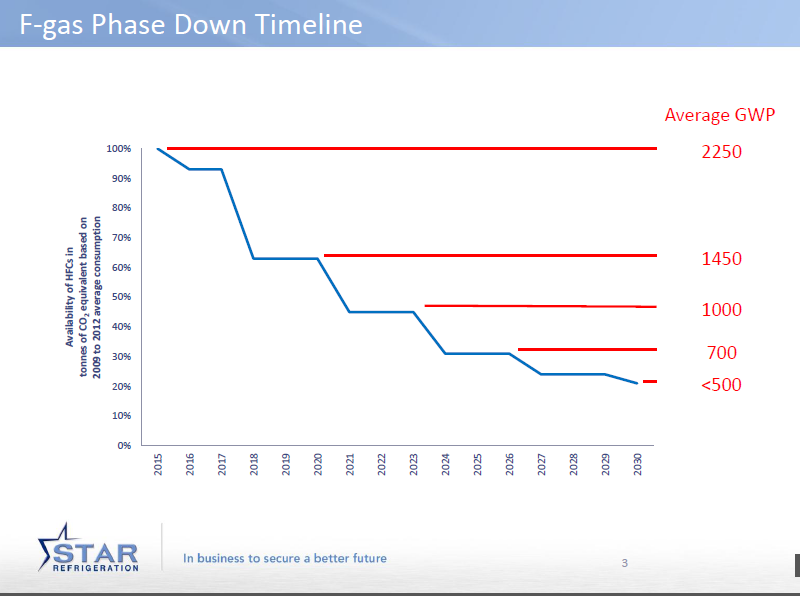

The latest revision includes a phase down programme that aims to reduce the use of high global warming refrigerants. The volume of refrigerant that can be sold across Europe is no longer measured in terms of kilograms but uses a metric of carbon dioxide equivalent. One kilogram of HFC refrigerant can be thousands of times more potent as a global warming gas that carbon dioxide. Starting in 2015, the timeline aims to reduce the tonnes of carbon dioxide equivalent from 100% of average levels measured between 2009 to 2012 to 21% by 2030.

At the beginning of 2016, the EU imposed an initial reduction of 7% in f-gases placed onto the market based on carbon dioxide equivalent. The biggest reduction took effect in January 2018, when the level dropped to 63% of the original benchmark. Moving away from substances which have a higher global warming potential (GWP), helps the EU in meetings its environmental targets..

In the UK, the government is set to remain aligned to the EU F-gas regulations and European safety standards post Brexit.

Also, The Kigali Amendment to the Montreal Protocol, an international agreement to phase down the production and use of HFCs, received the required ratification threshold of 20 countries and is now a legally binding protocol which entered into force on 1 January 2019.

The phase down isn’t refrigerant specific but looks at overall CO2 across all gases manufactured. This will encourage manufacturers to move to lower GWP gases in order to produce the same kg/yr

If you look at what the phase down means in terms of average GWP in the market – in 2015, if you take the total refrigerant sold, it equated to GWP of 2250; R134a is the most common single fluid used and is about 1400. R404a is probably the most common low temperature mixture used and it has a GWP of approximately 4000. If we take the benchmark as 2250 and take the same quantity of refrigerant as we go through the phase down timeline, by 2018 we would need to be down to an average GWP of 1450, in other words, everything that we use on average would need to be the same as R134a.

As we progress further, by 2023 it will be down at 1000 and at less than 500 by 2030. There are very few refrigerants that are widely used to date with a GWP less than 1000.

Therefore, to achieve these targets set on the graph we can move forward in two ways:

We can’t stop using refrigeration as it is a key requirement for many aspects of our daily life (e.g. food production and storage, data storage, beverage production, pharmaceutical production etc).. We need to look at alternative fluids that can be used for refrigeration, both naturally occurring and synthetic.

However, there are challenges in transitioning and adopting these new fluids:

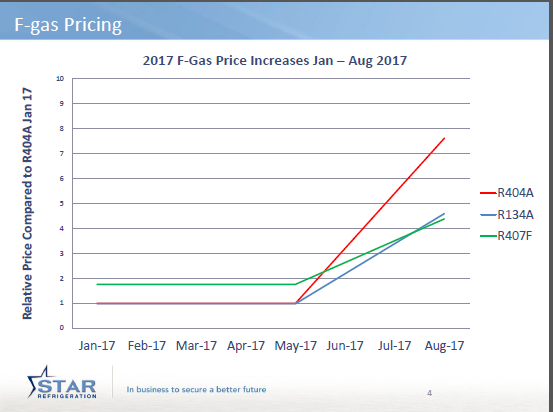

F-gas refrigerant prices are rocketing – for example, the price of R404a has increased over 700% in the last five months. This wasn’t the case for CFC or HCFC (R22) phase out and it is already causing concern within the industry as to how high prices will go and when increases will stop.

Leakage rates costs are also a big problem for businesses with refrigeration needs, as the cost of 1kg of refrigerant is now greater than the cost of 1 hour of a technician’s time to go and repair the leak. As the cost of refrigerants increases, contractors also have to put up their prices and pass on the hike to customers. This switches the focus to making synthetic refrigerant systems leak tight but in older distributed systems that have been in used for many years, leakage rates run in the order of 5 to 10% of the total content of the plant per year. On the other hand, new investment in new plants also has it challenges because if the contractor is being asked to supply the refrigerant, the cost of the gas that is going into the plant is probably multiple times higher than the profit the contractor is going to make in the job. If there is any issue during the commissioning of the system and a loss of refrigerant occurs, that is his total life hood gone. This is actually making contractors reluctant to propose HFC systems because of the increased risks.

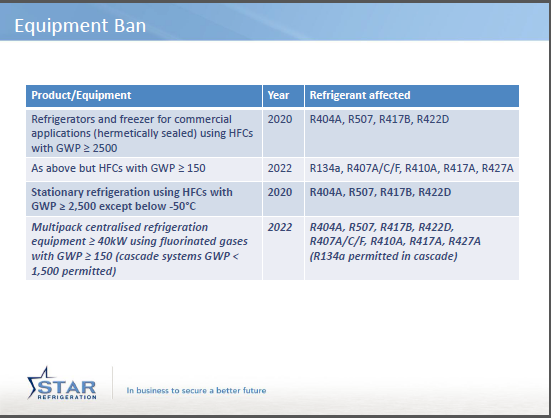

Equipment Ban

From a service point of view, restrictions on servicing equipment with high GWP come into play from 2020 onwards – this means that if you have a leak on this type of system, you would not be allowed to refill it with the same gas which is being phased out.

A key thing to remember is that it is very difficult to introduce a regulation like F-gas, but once the regulation exists, it is very easy to amend the numbers. The reason changes are likely to happen is that this is what has already happened with the CFC and the HCFC phase down.

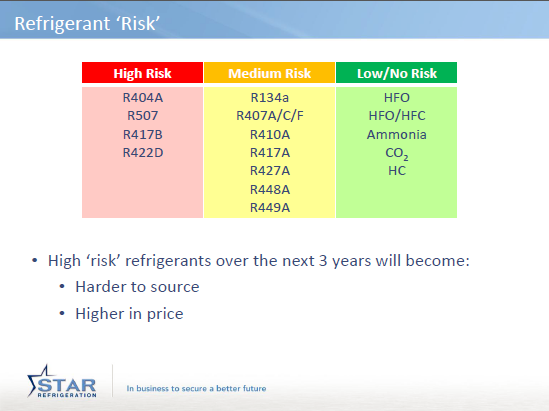

High risk fluids

If you have high risk refrigerants in your plant, then you have to change something in the near future, or you run the risk of your cooling system not being available to you as it can’t be maintained. These refrigerants are already becoming harder to source and expensive to purchase, so it’s best to plan ahead for the future and transition as soon as possible.

If you’re using the medium risk refrigerants, then it’s OK for now but you should expect to make changes in the next two to three years to stay compliant with the regulations and protect your business for price increases and reduced availability. If you’re using a low or no risk refrigerant, you’ve protected yourself from the regulations.

For those using refrigeration systems with high risk fluids, the next step should be to try and move from them to medium risk, or medium risk to low risk in order to be as prepare as possible.

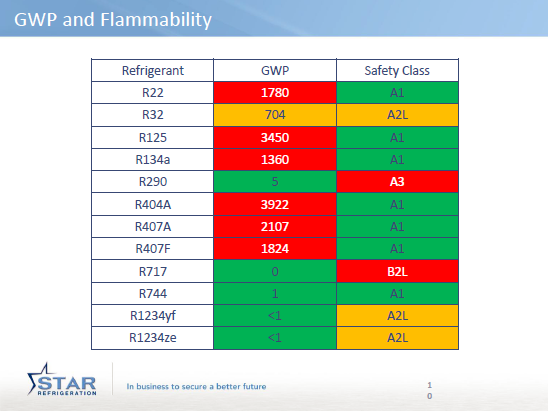

Flammability

Moving from high GWP to low GWP refrigerants is a complex process, and one of the challenges is flammability. Many gases are fantastic from a global warming point of view, but it is the flammable characteristics of the gas which brings its own safety difficulties.

Propane can be used safely in small systems such as domestic refrigerators or an outdoor air cool chiller plant, yet it wouldn’t be feasible for a split air conditioning system. Similarly, ammonia has a toxicity level to consider, so it could be used in a larger chiller but again not for an air conditioning system in an enclosed space.

Looking at the graph above, we see that in order to reduce GWP, we need to move away from A1 to the new A2L ‘mildly flammable’ classification or even A3. The only exception is CO2 which is a fire suppressant.

The next generation of low GWP, synthetic blends will be classified as A2L due to their high concentration of HFO or lower GWP HFO (e.g. R32). We need to accept this and develop systems to suit the flammability issue as with ammonia, however, we’ve been using ammonia for over 100 years.

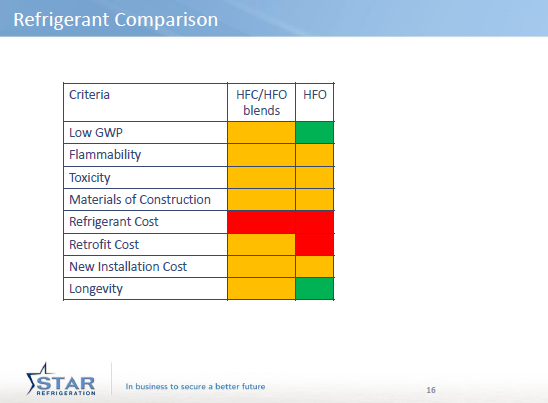

Refrigerant replacement options

What are HFO blends?

HFOs are fluorocarbons which breakdown quickly if released into the atmosphere, therefore they don’t have a big impact on global warming. When using HFOs you can use copper piping of the same pressure ratings and compressors so you won’t have to install whole new systems. On the other hand, these refrigerants are flammable and expensive, and the prices are expected to increase. Here are some more of the benefits and challenges of the HFOs.

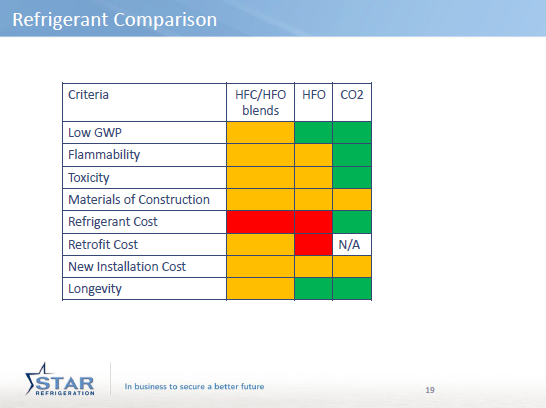

Carbon dioxide

Since the early 1990s carbon dioxide has become readopted as a refrigerant, especially in supermarkets. As well as having low GWP, it is also cost effective and very safe to use. The life of industrial CO2 systems will last as long as any other industrial system. The first one installed by Star was installed in 1999 and has since been in operation. The only disadvantage is that it is not possible to retrofit.

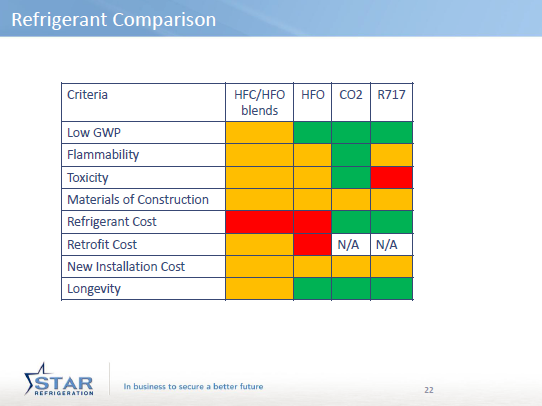

Ammonia

If you are looking for industrial type refrigeration, ammonia is a viable refrigerant to transition to. It’s a cost effective way to switch, and is the only refrigerant on the table with zero global warming potential. It’s widely available and very low cost, but the equipment and installation costs are likely to be higher. As a toxic gas you also need to understand the safety implications.

There is no single solution – there are plenty of options and opportunities provided by the f-gas phasedown. CO2 and ammonia are currently experiencing growth and they’re moving into areas they wouldn’t have been used before. It is possible to convert your plant and make it more efficient than it was before with a new choice of gas, especially as the cost of HFC refrigerants continuous to increase.

This article has been certified for Continuing Professional Development (CPD) by CIBSE and The CPD Certification Service. To get your CPD Certificate please email your request to CPDCertificate@star-ref.co.uk